In today’s fast-paced world, managing multiple debts can often feel like juggling too many balls at once. As of 2025, one practical solution gaining widespread popularity is debt consolidation using personal loans.

What Is Debt Consolidation?

Debt consolidation, in essence, involves combining several existing debts into a single loan with potentially more favorable terms. This strategy can simplify your monthly payments and even reduce the total interest you pay over time. According to The Hans India, this method is ideal for those struggling with multiple EMIs.

For instance, imagine you have three credit card debts each with different interest rates and repayment dates. Instead of juggling these payments every month, you could consolidate them into one loan from a financial institution like fastlendgo.com.

Why Personal Loans Work Best for Consolidation

A personal loan offers several advantages over other types of consolidation methods. Unlike secured loans that require collateral, such as a car or home equity, a personal loan is unsecured, making it easier to qualify for.

- Predictable Payments: A fixed interest rate ensures your monthly payments remain constant over the term of the loan. This makes budgeting much simpler and less stressful.

- Flexibility in Repayment Terms: Personal loans offer various repayment periods, allowing you to choose a tenure that fits within your budget while minimizing overall interest costs.

- Digital Convenience: Many lenders today, like IDFC FIRST Bank, provide a seamless digital experience with swift disbursals and paperless processes.

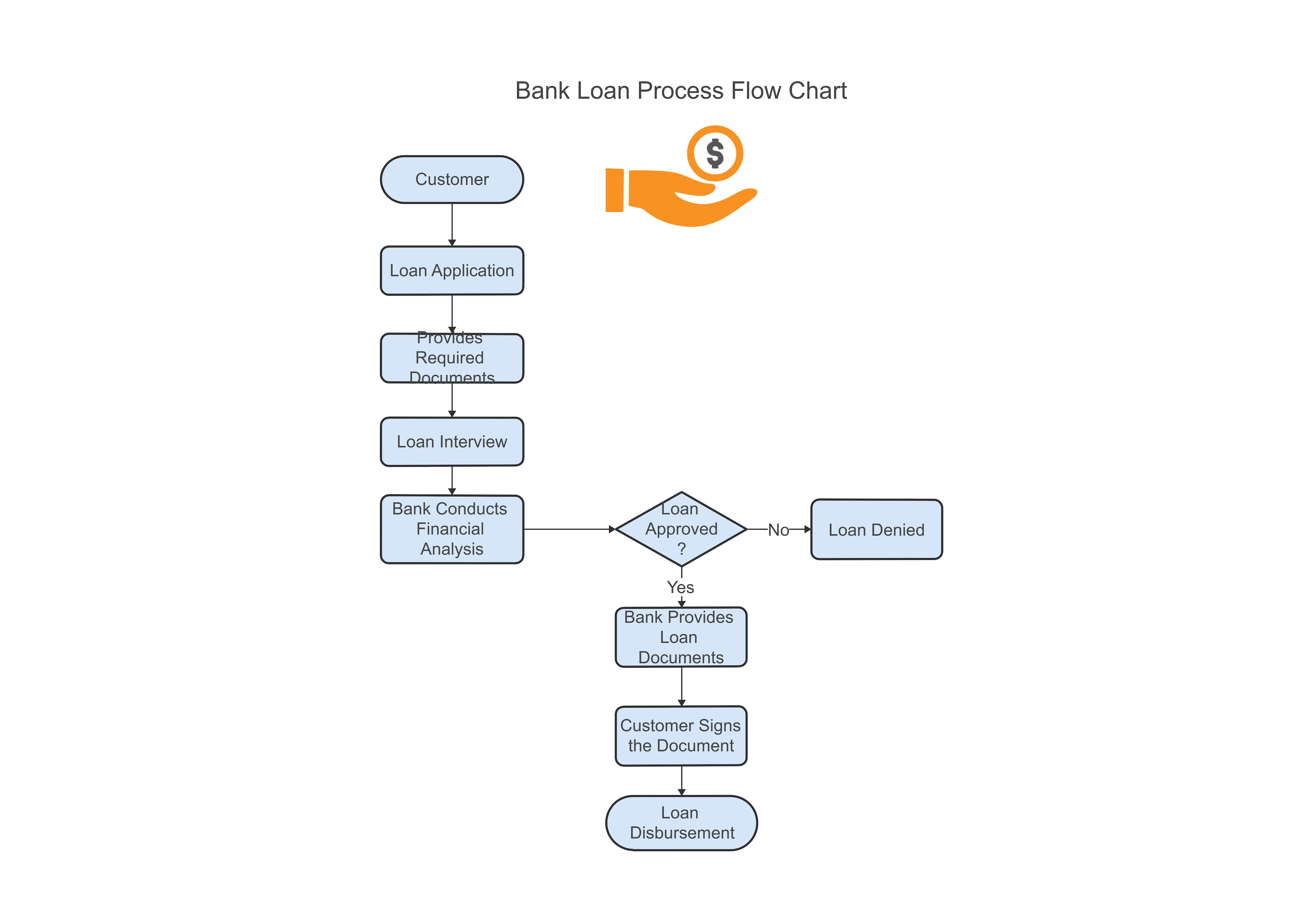

Steps to Consolidate Debt Using Personal Loans

To effectively consolidate your debts, follow these steps:

- Evaluate Your Current Debts: Gather all relevant financial information such as interest rates, monthly payments, and due dates. This will help you determine the total amount needed for consolidation.

- Check Your Credit Score: A strong credit score can improve your chances of securing better loan terms. Visit Credit Karma to get a free assessment.

- Research Lenders and Loan Offers: Compare different lenders based on their interest rates, fees, and repayment flexibility. Don’t forget to check for any hidden charges or penalties.

- Use an EMI Calculator: Utilize online calculators provided by reputable banks such as IDFC FIRST Bank’s EMI calculator. This tool helps estimate your monthly payments and total repayment amounts.

- Carefully Review the Terms: Once you have a list of potential lenders, carefully read through their terms and conditions. Look for clauses related to foreclosure, part-payment options, and prepayment penalties.

- Apply for Consolidation Loan: After selecting your lender, fill out an application form either online or offline. Provide all necessary documentation such as proof of income, identification, and recent bank statements.

Borrow Only What You Need

One critical mistake to avoid is borrowing more than you actually need for consolidation. This can lead to increased interest costs and potentially set back your financial goals. Remember:

- No Margin for Renewed Spending: Consolidation should simplify, not complicate. Stick to the amount needed to clear existing debts.

- Set Up Auto-Debit or Reminders: To maintain a good credit score and avoid late fees, set up automatic payments or regular reminders to ensure timely repayments.

Evaluating Debt and Credit Before Applying

Before you apply for a personal loan, take some time to thoroughly assess your current financial situation. This includes:

- Listing All Outstanding Debts: Document each debt along with its billing cycles, interest rates, and due dates.

- Stress-Testing EMIs with Calculators: Use online calculators to run various scenarios adjusting both the amount borrowed and repayment tenure. This helps you understand how changes might affect your monthly outgo.

The Importance of a Clear Consolidation Plan

A well-planned consolidation strategy not only simplifies your finances but also sets you up for long-term financial health:

- Build a Roadmap: Create a step-by-step plan mapping every existing debt and the steps required to settle it through consolidation.

- Select Sustainable Tenures: Choose repayment tenures that align with your cash flow without stretching your budget too thin.

- Closing Old Credit Lines Properly: Once the new loan is disbursed, ensure you obtain closure letters and updated statements from previous lenders to avoid any misunderstandings or missed payments.

Risk Checks You Shouldn’t Skip

To safeguard your financial health during debt consolidation, adhere to these risk checks:

- Guard Your Credit Profile: Maintain a disciplined repayment schedule and stay vigilant about any changes in the loan’s terms.

- Read Fine Print Regularly: Periodically revisit your lender’s website for updates on applicable fees, eligibility criteria, and process requirements. Being informed can save you from unexpected charges or penalties.

The Role of Reputable Lenders

Selecting a reputable financial institution is crucial when considering debt consolidation through personal loans:

- IDFC FIRST Bank Example: Known for its transparent terms, flexible repayment options, and swift disbursals, IDFC FIRST Bank offers competitive interest rates with zero foreclosure charges. Their 100% paperless process ensures a hassle-free experience.

Maintaining Financial Discipline Post Consolidation

After consolidating your debts into one loan, it’s essential to maintain discipline and stay on top of your finances:

- Organize Closure Documents: Keep all closure letters and updated statements from previous lenders organized and accessible. This helps in verifying that old accounts have been properly closed.

- Monitor Credit Profile: Regularly review your credit report for any inaccuracies or discrepancies that could impact your financial standing.

Final Thoughts on Debt Consolidation Using Personal Loans

Debt consolidation through personal loans can be a powerful tool in simplifying your finances and making repayment more manageable. By choosing the right lender, carefully structuring your loan plan, and maintaining discipline throughout the process, you can achieve financial clarity and peace of mind.

Comparison with Other Options

While debt consolidation using personal loans is a popular method, other options like home equity loans or balance transfers might be suitable for some individuals. However, these alternatives often come with additional requirements such as collateral or high fees that may not align well with everyone’s financial situation.

Real-Life Examples

A common scenario involves someone who has multiple credit card debts with varying interest rates and payment due dates. By consolidating these into one personal loan, they can streamline their monthly budgeting process and potentially reduce the total amount of interest paid over time.

In Conclusion

Debt consolidation using a personal loan is a strategic move that requires careful planning and execution. By following the steps outlined above and choosing reputable lenders like IDFC FIRST Bank, individuals can simplify their financial lives and work towards becoming debt-free more efficiently.

| Lender | Interest Rate (2025) | Repayment Flexibility | Suggested Tenure for Consolidation |

|---|---|---|---|

| IDFC FIRST Bank | Starting at 10.99% | Varying repayment options available | Typically 2 to 5 years, depending on financial needs and capacity |

Note: These figures are indicative and may vary based on individual creditworthiness.

Contact Us for More Information

If you’re considering debt consolidation using a personal loan in 2025, reach out to fastlendgo.com for personalized advice and assistance. Their team of financial experts can guide you through the process and help you choose the best option based on your unique circumstances.

Remember, while debt consolidation offers a streamlined approach, it’s crucial to maintain discipline throughout the repayment period. By staying informed and proactive about your finances, you can take significant steps towards achieving long-term financial stability and peace of mind.

Stay tuned for more tips and insights on personal finance management from our team at fastlendgo.com!